Steve Roth comments:

And there's no such thing as "money in circulation" at any given moment. That pipe going out of and back into the money bathtub is instantaneous.

It's either in this account, or it's in that account. It's never in between, or in transmission.

There is not money out there on the highway as there are cars.

Money doesn't actually "move." There are only changes in the tallies on balance sheets. (Dollar bills are just physical tokens representing balance-sheet tallies. [See R Wray on the origins and nature of money.])

It's on this balance sheet, or it's on that balance sheet.

It's either in this account, or it's in that account. It's never in between, or in transmission.

There is not money out there on the highway as there are cars.

Money doesn't actually "move." There are only changes in the tallies on balance sheets. (Dollar bills are just physical tokens representing balance-sheet tallies. [See R Wray on the origins and nature of money.])

It's on this balance sheet, or it's on that balance sheet.

"It's on this balance sheet, or it's on that balance sheet," Steve says. But how does it get from this balance sheet to that one? At last we have hit upon the difference between accounting and economics:

Economics deals with forces that change balance sheets.

Adam Smith comments:

The gold and silver which can properly be considered as accumulated or stored up in any country may be distinguished into three parts: first, the circulating money; secondly, the plate of private families; and, last of all, the money which may have been collected by many years' parsimony, and laid up in the treasury of the prince.

There is money we plan to spend, and money we plan not to spend. The former is in circulation; the latter is savings. It's that simple. The Federal Reserve defines this clearly on the "notes" tab for the M1SL series:

M1 includes funds that are readily accessible for spending.

The M1 number, the funds that are readily accessible for spending, is probably a little more than the amount of money people plan to spend, because everybody wants to save a dollar. The spending-money I have, that gets me through the week, I don't want to be broke on payday, I want a few bucks left over. Anyway...

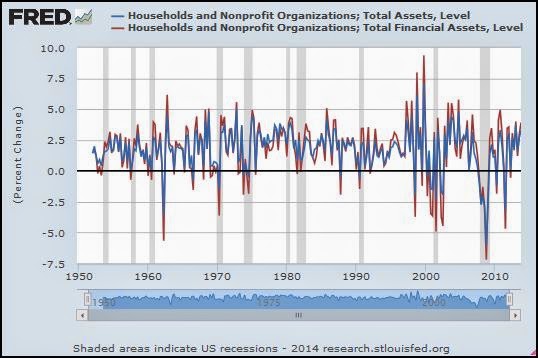

Suppose we take total outstanding debt as a measure of total outstanding money. (This is somewhat like Steve Roth saying that the total value of assets is money.) Accumulated debt is a measure of money that exists, somewhere, that borrowers are still paying interest on because they didn't pay off the debt yet, they didn't extinguish the money.

So we can take the funds available for spending -- FRED's M1SL -- and compare that number to accumulated debt as a proxy for the total amount of money that exists, that people are paying interest to maintain in existence, FRED's TCMDO:

|

| Graph #1: M1 -- the money we use to pay off debt -- per dollar of debt. |

Every dollar of that debt corresponds to a dollar of money that was newly created when the debt was created. The debt still exists. So where is the other 96 cents?

A lot of it went into savings and other financial assets, and out of circulation.

There's a big focus these days on income inequality. Here's the root of the problem: Some people are earning interest and others are paying interest on more and more and more of the money in our economy. It's a mad house! A mad house!

The graph shows there's only four cents left, with which to pay the interest and principal on a dollar of debt and still do everything else we need money for.

And paying off a dollar of debt reduces that four cents by a dollar.